Introduction

by Tim Gramatovich, CFA.

Chief Investment Officer

On November 5th, 2024, the world as we knew it changed. Donald Trump was elected for a second time with no ambiguity on where he wants to lead the US so make no mistake; this is not the historical Republican party but an entirely new force which is about to reshape the globe, particularly as it relates to trade.

Export driven economies such as China, Canada and Mexico and parts of the EU are very exposed. Canada is likely to suffer a significant amount of collateral damage from a protectionist America. It will not help that the current Canadian government is in turmoil.

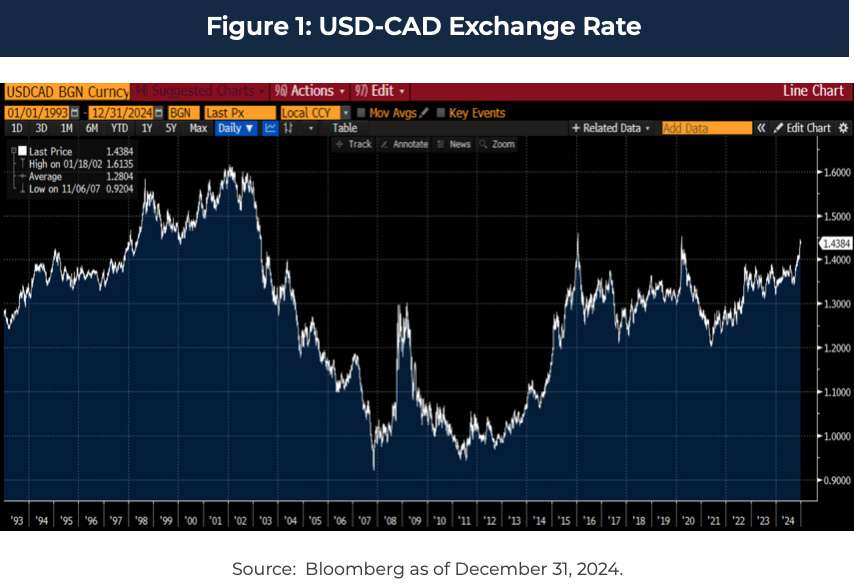

The Canadian economy has been dramatically underperforming the US, and this is likely to get worse. Growth, productivity and consumer debt are all headed in the wrong direction. This is partially reflected in the current exchange rate.

To those who think $0.69 is overdone — go back to 1998 where the currency spent half a decade in the $0.60s finally bottoming at $0.62 in 2002 (i.e. $1.61 CAD to USD). The present and future environment look far worse, so an all-time exchange rate low is probable.

“To me, the most beautiful word in the dictionary is tariff,

and it’s my favorite word.”

— President Donald J. Trump

That was a direct quote from President Donald Trump back in late October during a Bloomberg interview.

On Monday November 24th, Donald Trump backed that up by announcing a 25% tariff on all goods and services coming into the US from Canada and Mexico.

The rationale was illegal immigration and fentanyl. Canadians were taken aback given the very limited amount of either of these issues emanating from the Canadian border.

The initial response was that this was nothing more than posturing to begin negotiations. I would caution Canadian investors that this is more than likely not the case.

President Trump does not view tariffs as a means to an end but an end in themselves. The goal of this administration is to use tariffs as income to pay for an extension of tax cuts in the US and to force more onshoring of production inside US borders.

This was echoed in a recent Economist article entitled “Tariffers vs Traders.”

“There are big questions, too, about whether Mr Trump sees tariffs as a means or an end. His defenders insist that tariffs are a negotiating gambit. Yet in Washington, those same levies are starting to sound worryingly permanent. Republicans in Congress are enthusiastic about using revenues from tariffs to “pay for” cuts to taxes on income or corporate profits, the forum heard. Advocates argue that the first Trump administration carefully imposed preventive tariffs on industries in which American firms still have an edge, but which China has in its sights.”

— The Economist

Understanding Global Trade

America has significant trade deficits with almost all of the major economies including China and the EU. While the pie was growing for all parties, this was tolerated. This is no longer the case.

According to the US Bureau of Economic Analysis, September 2024 deficits (latest data in billions of dollars) were recorded with China ($26.9), European Union ($23.8), Mexico ($16.0), Vietnam ($12.2), Ireland ($9.3), Taiwan ($7.0), Germany ($7.0), Canada ($5.7), South Korea ($5.7), Japan ($5.3), India ($3.4), Italy ($3.4), Switzerland ($2.3), Malaysia ($2.1), France ($1.1), Israel ($0.8), and Saudi Arabia ($0.2). Most of these countries are in the cross hairs of US trade policy.

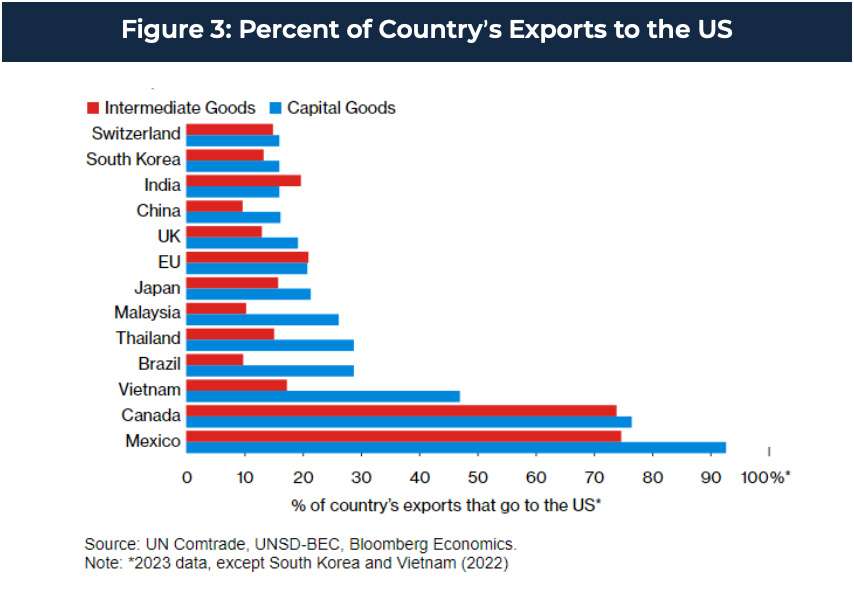

There is considerable misunderstanding when it comes to Canada-US trade and the nature of the two economies. Canada’s GDP is about $2.2 trillion while the US is $30 trillion.

The US now has five companies with a market capitalization of more than Canada’s entire GDP of $2.2 trillion (Amazon, Alphabet, Apple, Microsoft and Nvidia). Canada is an export driven economy with exports accounting for 34% of GDP with approximately 80% of those exports heading to the US.

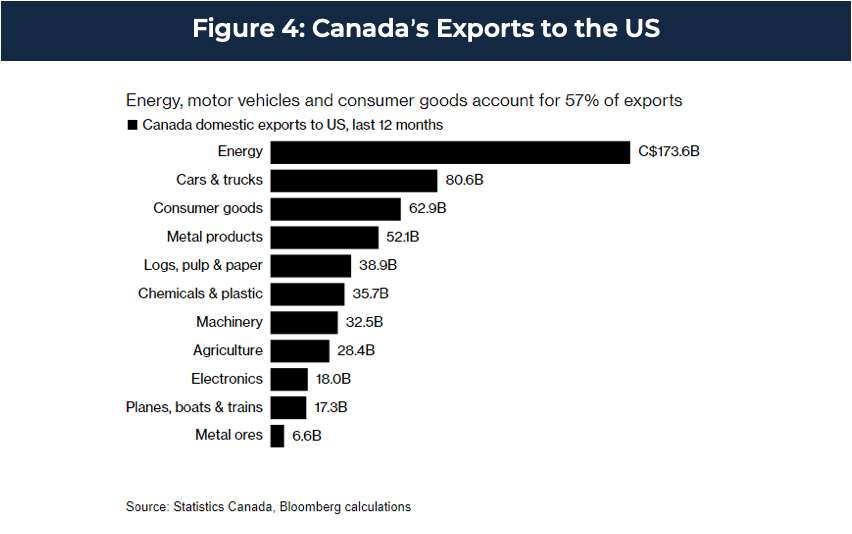

Since President Trump is a consistent supporter of the oil and gas industry, there is a “feeling” (or more accurately hope) that there will be a tariff exemption on Canadian energy.

I think this is misguided.

While the US needs heavy oil production, they also know that there is nowhere else for this landlocked oil to go. While 25% may not be the number, tariffs or a negotiated discount are coming. The idea that this would cause energy prices to soar is also specious.

Why won’t the refiner bidding for crude lower their bid?

Canadian energy will be expected to subsidize a percentage of the finalized number and will feel the pain which then reverberates throughout the domestic economy.

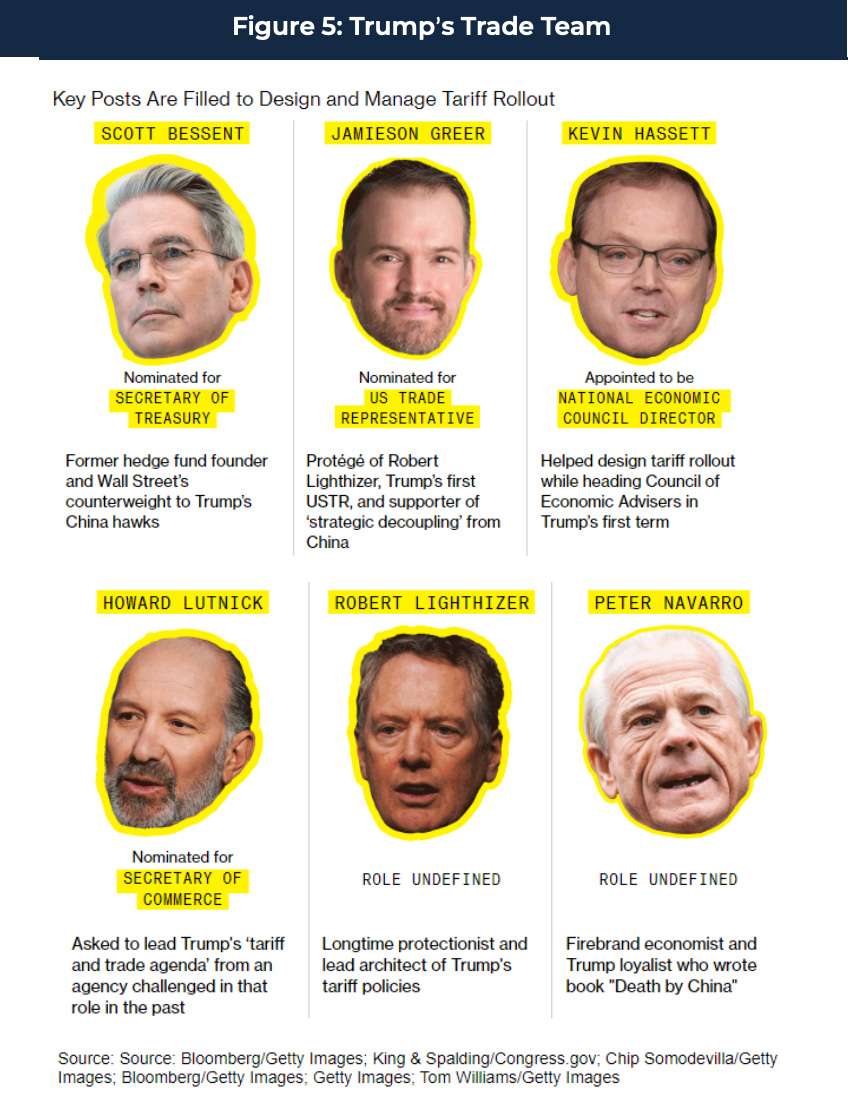

The US trade team is filled with true believers on tariffs and are in place to support Trump’s agenda, not bring balance to the force:

While some countries may try and play hardball, there is no credibility to threaten the US with retaliatory tariffs as only 10% of US GDP is linked to exports.

US exports to Canada amounted to $350 billion or slightly more than 1% of US GDP. US GDP is now almost 80% services — further insulating the economy from any trade wars, so this is truly a one-way negotiation.

President Trump’s trade and economic team share a common belief that America has been taken advantage of by its Allies in two distinct areas — trade and defense.

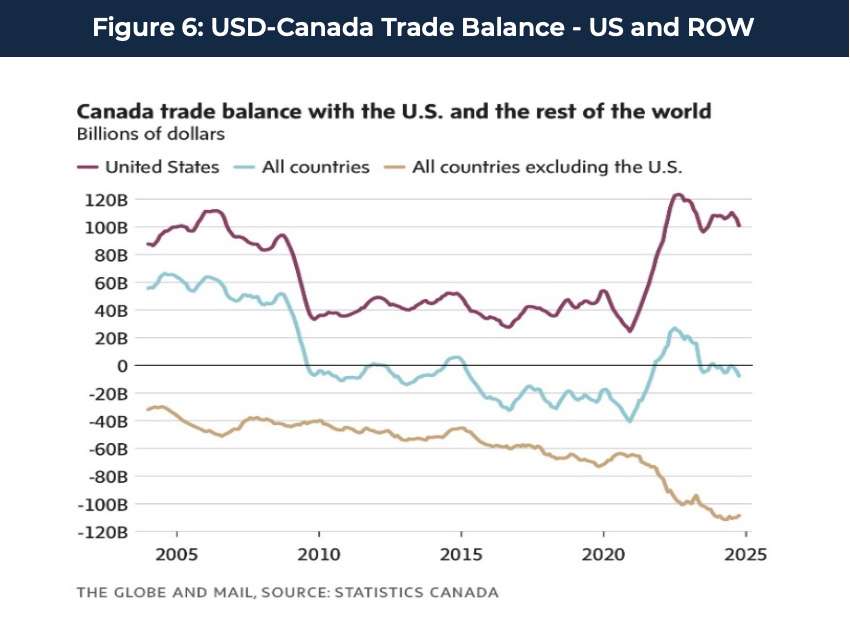

Canada is a poster child for this with a trade surplus of approximately $8 billion per month and defense spending nowhere near the NATO commitment of 2% of GDP.

President Trump has already mentioned that Canada “is ripping off the US to the tune of $100 billion.”

The Canadian Economy

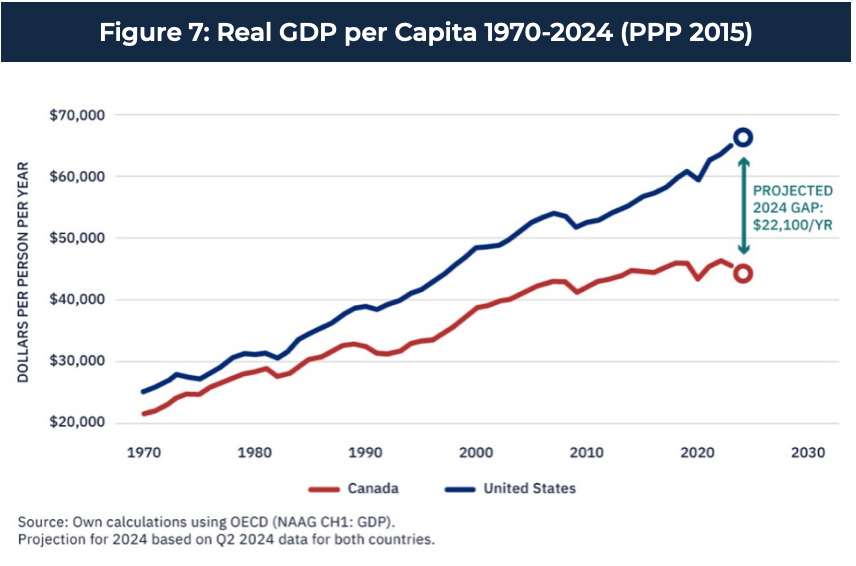

To say the Canadian economy has underperformed against the US would be a dramatic understatement. Q3-2024 marks six straight quarters where Canada’s economy has fallen below population growth.

GDP per capita in Canada is on track to be 50% below that of the US which is the widest level in over a century.

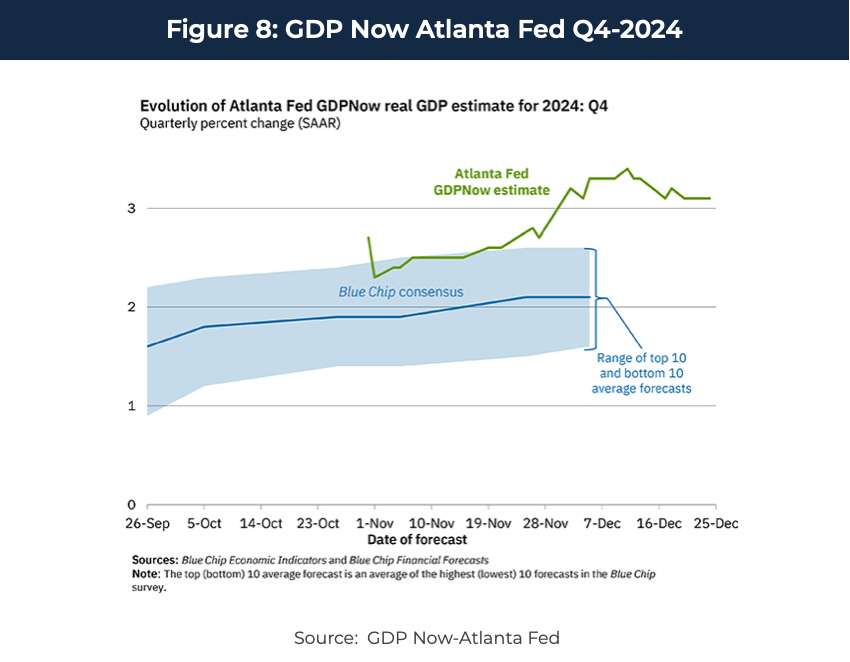

Annualized Canadian GDP in the 3rd quarter came in at 1.0% vs the US at 3.1%. Recent data forecasts for the US in Q4 are for 3%+ annualized growth and we expect to continue to see a divergence in economic growth between the two countries.

There is nothing on the horizon that suggests these gaps will close. If anything, American trade policy will exacerbate the under-performance.

Canadian GDP Breakdown

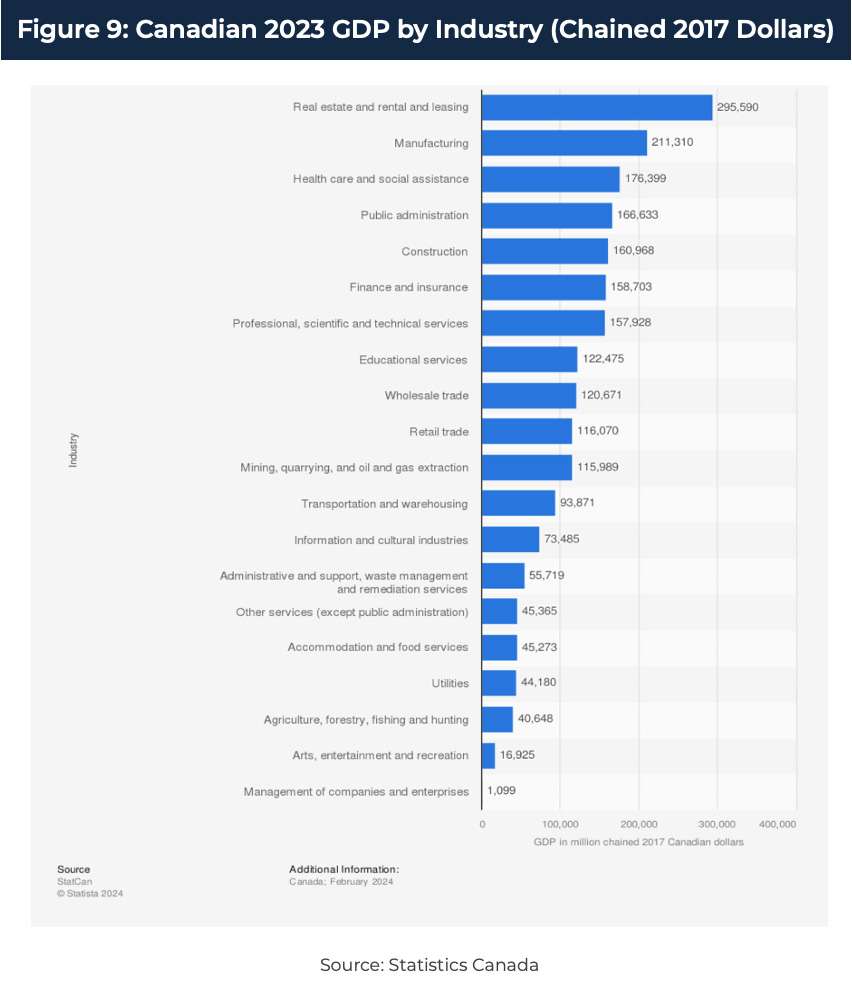

The news continues to deteriorate as we break down the Canadian economy. Real estate has become the dominant contributor to GDP in Canada.

According to StatsCan — real estate is about 15% of GDP. However, note that construction is an additional 8%. Since we do not have a breakdown of this category it would seem probable that a percentage of this amount is also dedicated to residential real estate.

It would not be a stretch to assume over 20% of Canadian GDP is directly or indirectly related to the real estate sector.

Not to be outdone, government (Healthcare and Public Administration) is another 15%+ of GDP.

The problem is that both government and real estate are non-producing assets from an economic perspective.

To put an exclamation on this point, November employment data in Canada showed an increase of 51,000 jobs, with 90% of those being created by the public sector. This did not stop the Canadian unemployment rate from rising to 6.8%.

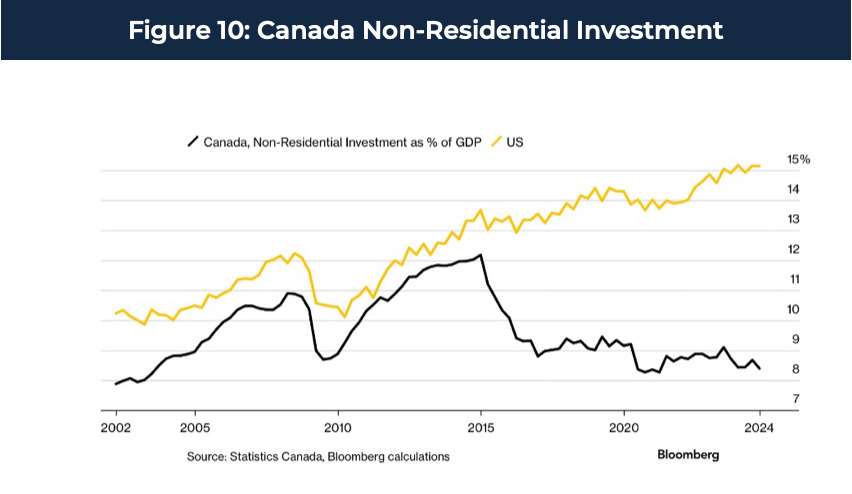

Productive spending, as measured by business investment, has plunged over the last 10 years and is now about 50% of the US as a percentage of GDP.

Consumer Debt

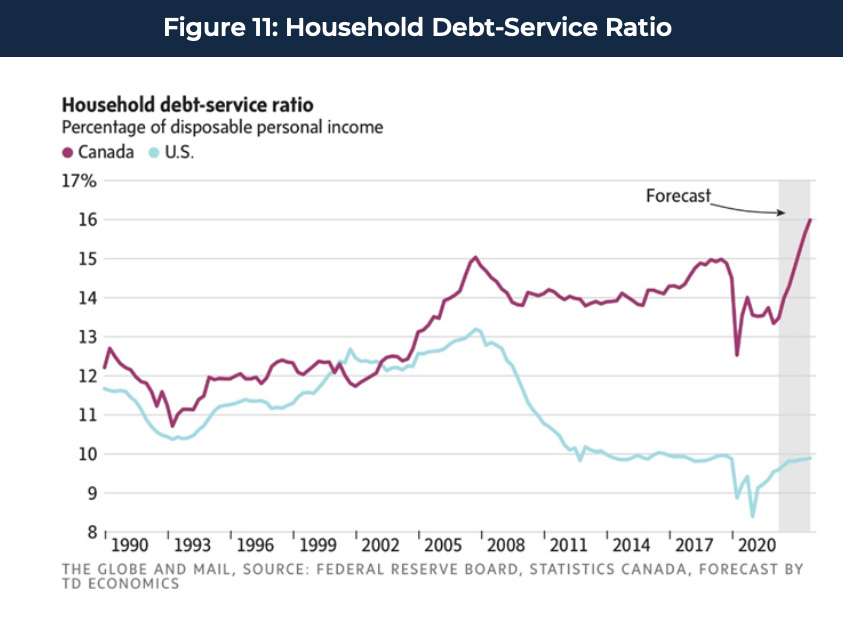

What makes the story even worse is that this economic malaise was accompanied by massive debt accumulation.

Canadian consumer debt has exploded over the past 20 years which has led to a very large divergence between US and Canadian households. Note that even at the peak of the financial crisis in 2008, Canadians spent more disposable income on debt service than Americans.

Since that time, the US consumer has continued to de-lever while Canadians have continued to accumulate debt.

The bulk of this debt consists of mortgage debt. Existing US mortgages are almost entirely 30-year fixed rate which have not been impacted by the Fed rate hiking cycle starting in 2022.

Canadian’s have gorged on variable rate mortgages as this tended to be the cheaper monthly payment at time of origination and fixed rate mortgages are usually 5 years or less in maturity.

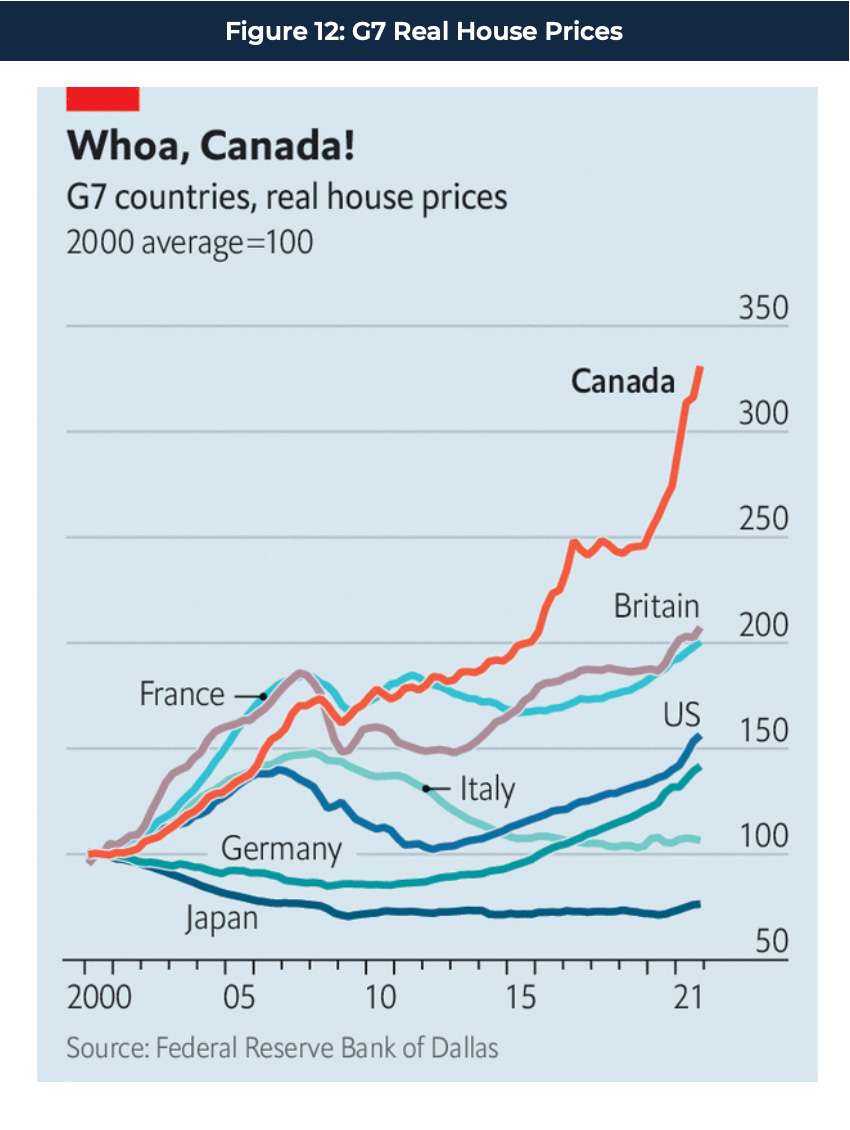

As stated, real estate has no multiplier effect on the economy except creating further speculative behavior. In a world filled with asset bubbles, Canadian residential real estate is arguably one of the largest today.

This is the home affordability of the 25 largest cities in North America with Vancouver and Toronto topping the list with an absurd double-digit ratio.

There is no tax deductibility of mortgage interest in Canada so trying to find an explanation remains challenging. The common refrain remains inventory and immigration. We find that explanation underwhelming as recent immigrants are highly unlikely to be bidding (i.e. qualify) for $800,000+ homes.

Yield Spreads and Currency

How does all of this current and forecasted economic data impact investors in the real world? The Canadian economy is weak and is highly dependent upon real estate.

Both suggest significant additional cuts to rates in Canada beyond the 50 bps cut in December of 2024. With US GDP growth coming in around 3%, the Fed has already signaled reduced rate cuts coming into 2025.

If inflation remains stubborn in the US, the market could pull currently priced in Fed rate cuts out of the curve entirely. Vice-versa, with the market only pricing in two 25 bp cuts for 2025 in Canada, additional cuts could be added to market expectations as economic weakness comes to fruition. The interest rate differential will continue to widen which causes CAD to fall as investors leave CAD and move to USD in search of better yields.

The current yield spread between Canadian and US 10-year Treasuries is over 130 basis points which is the highest in at least 35 years. This will continue to drive investor money out of CAD and into USD.

Conclusion

The “Business of America is Business” stated Calvin Coolidge in a 1925 speech and it appears this is once again a driving force. There is going to be considerable collateral damage as the US radically changes policy from global defender and free trader to MAGA. And, again, this isn’t just a MAGA movement, there is support across the political spectrum in the US for major changes in international trade.

Much of the developed world is in complete chaos including Canada, Germany (leadership failure and a recession), France (failed government), Britain (4 Prime Ministers in 5 years) and South Korea (Marshall law).

Outside of price appreciation from a massive real estate bubble, there is very little good news for the Canadian economy and by extension the currency in all this chaos. This dramatic underperformance in both areas has come during a relatively benign relationship with the US. There should be little doubt that this is going to change for the worse. The economy is likely to experience stagflation as growth grinds to a halt and CAD continues to weaken with a very dovish Bank of Canada slashing rates.

This increases the price of key imports (i.e. food), causing further pain to consumers. Canada’s massive tax disadvantage is likely to get worse with further cuts in the US and its experiment with carbon taxes makes the country less competitive.

All of this tends to drive people and business south. While a change in Federal Government leadership for Canada in 2025 is likely, the issues surrounding Canada are structural not cyclical.

Currency markets tend to move in long term cycles and there will be two very different economies starting with this next presidential term and extending into the coming decades.

There will be no easy fix for Canada, and we expect another significant leg down in the currency.